In the absence of sufficient activity data at sector level to carry out a financial impact assessment, consolidated data from Climate Action Accelerator’s humanitarian partners has been used to provide a picture of the financial impact of implementing climate solutions in general. For this analysis, financial data from nine Climate Action Accelerator’s partners was used. These organisations, which vary in size and are involved in different activities, represented approximately 9% of the international humanitarian assistance budget (in terms of financial expenditure) in 2022.

Although not fully representative of the sector, this sample size is relevant enough to establish trends and benchmarks. The analysis below shares lessons from organisations who have used similar, comparable, and systematic approaches to set quantitative targets and estimate related costs, savings and investments. To our knowledge, this is the only available sample in the humanitarian sector today.

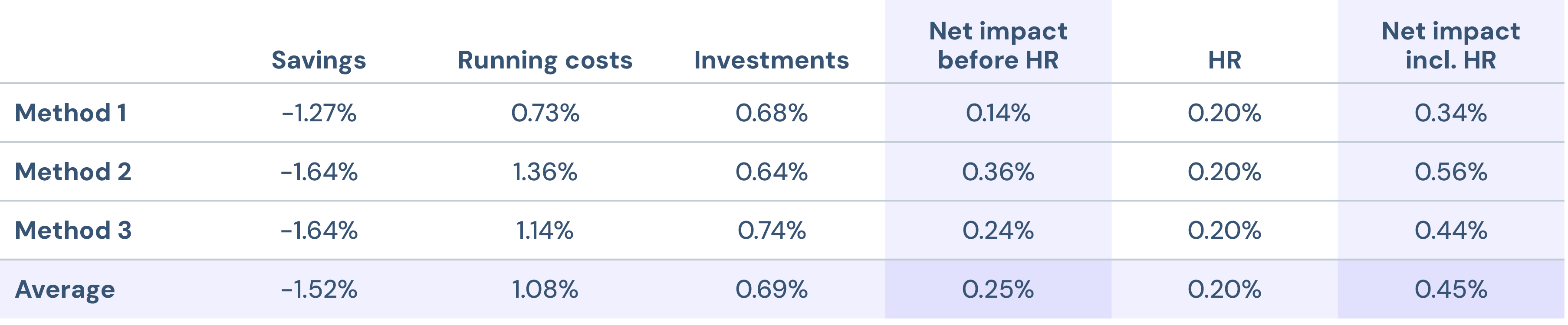

Even though they were originally established over different periods of time, the roadmaps were all extrapolated over a seven-year period to improve comparability. Three different extrapolation methods were used to model missing data from year 4 to 7 and improve the comparability of results. All three approaches calculate average savings, running costs and investments as a percentage of the organisations’ yearly budget.

No extrapolation was undertaken for the impact of environmental solutions and human resources costs, the respective available averages of 0.16% and 0.20% were therefore used for all three methods. The data in the following analysis is the average of the three methods, as detailed below.

The full methodology and sample are detailed in Appendix 5.

Table 2: Average savings, running costs, investments and net costs, Climate Action Accelerator’s consolidated partner data